I must be getting old.

Know how I know? Friends of mine don’t send me new music these days. They just send me viral videos.

Today so far, I’ve snickered, mesmerized, ooh, perhaps 31 times at Democracy Manifest Man.

The other video link I’ve received? Robert Plant performing Stairway To Heaven, for the first time in 16 years, in the relatively teeny venue of Soho Farmhouse (UK).

The crowd in that video surely knows, down to their bones, that they should be stood in hushed reverence. After all, they might be witnessing the last ever time that King Zep, 75, belts out his most universally cherished song.

But do you know what some people in that crowd do? They actually sing along. Lost in the moment, they tunelessly echo back Plant’s words, rather than basking in them. They can’t help themselves.

Watching this tableau – people giddily parroting a scintillating chorus, no matter how inapposite doing so might seem in hindsight – reminded me a little bit of the music industry and Merck Mercuriadis.

Over the past month, I’ve listened to several, let’s say, Mercuriadis skeptics (he’s on quite a lot of rivals’ dartboards, that guy!).

Often with some glee in their voices, these folks have daydreamed aloud how Hipgnosis Songs Fund‘s ‘continuation vote’ will become the moment their imaginary nemesis finally gets nobbled.

“It’s the day the house of cards finally falls down! The day the piper gets paid! The day Merck’s left ‘holding the bag’!” etc.

Well, as you probably know by now, that ‘continuation vote’ took place yesterday morning in London (October 26).

It was expected that a reasonable majority of Hipgnosis Songs Fund (HSF) shareholders, frustrated by the firm’s sagging share price and the shock recent slashing of their interim dividend, would vote against continuation.

This, though, was a landslide: Around 83% of HSF stockholders opted to reject ‘continuation’ – while also voting to immediately oust HSF’s already-exiting Chairman, Andrew Sutch.

The move has left the future of HSF hanging in the balance.

Yet far from spelling the end of Merck Mercuriadis (and the Blackstone-backed investment adviser he leads, Hignosis Song Management), Hipgnosis Songs Fund’s ‘discontinuation’ may yet play right into his hands.

In a second, I’m going to do a spot of my own “giddy parroting”, by paraphrasing in text some conversations I’ve had (and not had) with people this past fortnight about Mercuriadis and HSF, and their respective futures.

But for now, let’s hear from the man the whole industry’s talking about (again!)… via a statement that Mercuriadis issued in the wake of the discontinuation vote from HSF shareholders.

“[Yesterday’s] Hipgnosis Songs Fund AGM marks an opportunity to reset and focus on the future. Our conversations with shareholders have revealed a consensus that they are enthusiastic about the quality of [HSF’s] iconic portfolio of songs.

“However it is also clear that they are asking for change and we respect that feedback. Hipgnosis Song Management’s new management team and I have already started taking the relevant necessary action to meet the expectations of shareholders.

“Our commitment to the Company’s shareholders remains absolute and we look forward to working with a new Chair and reconstituted Board during this period to ensure that the Hipgnosis Songs Fund delivers for its shareholders. During this process, shareholders can be certain that Hipgnosis Song Management will continue to manage the Songs with the greatest duty of care as always.”

Mercuriadis also thanked Andrew Sutch, as well as non-exec directors, Andrew Wilkinson and Paul Burger – who both fell on their swords ahead of yesterday’s vote – for their service.

So: what happens now? Is Mercuriadis really fried? And how on earth can it be possible, post-HSF’s discontinuation, that he’s left “holding all the cards”?

To explain, enjoy this writer arguing with himself in eight easy steps…

Step 1: What a thumping loss for Merck! 83%! Does he now get ousted?

Not the smartest start to this conversation.

A ‘continuation vote’ – which all investment trusts on the London Stock Exchange legally have to hold every five years – doesn’t mean the immediate end of a fund. Nor does it mean the immediate end of that fund’s relationship with its investment adviser.

Yesterday, in a note to investors, JP Morgan’s Christopher Brown succinctly summarised what discontinuation actually means for HSF:

“In accordance with [HSF’s] prospectus, the Board is now required to put forward within six months proposals for the reconstruction, reorganisation or winding-up of [HSF]. These proposals may or may not involve winding-up [HSF] or liquidating all or part of the existing portfolio of investments.”

For the time being, HSF is maintaining its investment adviser – Hipgnosis Song Management (HSM) aka Merck Mercuriadis. Meanwhile, yesterday HSF shareholders re-elected three of the company’s Board Directors: Simon Holden, Sylvia Coleman and Cindy Rampersaud.

So as you read this, HSF still has a board, and still has an investment adviser.

The most pressing concern of that board? Finding a Chairman to replace the now-ousted Andrew Sutch.

Rumors suggest that a likely candidate to fill those shoes will be Rob Naylor, previously the Chairman of Round Hill’s UK royalty fund (which will shortly be the property of Concord).

Relevant: obviously, Hipgnosis Song Management (aka Mercuriadis and his team) also counts Blackstone-backed Hipgnosis Song Capital (HSC) as a client.

So even if HSF did manage to boot him out – which I doubt will happen, as I’m about to explain – Mercuriadis’s eggs aren’t all in one basket anyway.

Step 2: Right. but once the new HSF board’s in place, they’ll either (a) Fire Merck or (b) sell the company to someone else – someone like a major music company. He’s cooked!

Do you not read Music Business Worldwide?

Yes, to be clear, the Hipgnosis Songs Fund board can now turn around – as they’ve always been able to do – and fire Hipgnosis Song Management as HSF’s adviser.

That’s unlikely, though not impossible, for a few reasons.

Earlier this month MBW reported that Merck Mercuriadis had agreed to new concessions in HSM’s contract with HSF.

Even so, if HSF now fires HSM as its adviser, contractually HSM has a minimum 12-month notice period; HSF would also have to pay HSM an additional penalty.

Both of these things (the notice and the penalty), depending on the share price, I hear, could add up to somewhere in the region of GBP £15 million to GBP £25 million.

And then, the killer detail: As MBW reported last week, Hipgnosis Song Management and Merck Mercuriadis have an exclusive ‘call option’ in place to buy the entirety of HSF’s assets if HSM is ever terminated as HSF’s investment adviser (aka: if Mercuriadis is fired).

I will dig deeper into the solidity of that ‘call option’ – and why it matters more than you might initially appreciate – shortly.

A bigger question for now: what does HSF firing HSM actually gain the listed company in the short term? Other than momentarily pumping some blood through the capillaries of HSF shareholders angry about the current stock price?

As Mercuriadis said in his statement, HSF’s shareholders aren’t questioning the quality of the fund’s assets – with stakes in the songbooks of Neil Young, Shakira, Enrique Iglesias, 50 Cent, Lindsey Buckingham, Christine McVie, Jack Antonoff, Andrew Watt, and the Red Hot Chili Peppers, to name a handful.

Mercuaridis personally amassed this enviable portfolio for HSF, leaning on his unique contacts book. He did so across five years (2018-2022) when – other than a very small circle of others (hi Larry!) – Mercuriadis’ non-major-music-company competitors were rarely able to challenge the scale of premium-level assets that HSF swallowed up.

Yes, some will argue that Mercuriadis paid too high a multiple for certain assets (whether newer catalogs or ‘vintage’ catalogs).

But HSF shareholders clearly believe those catalogs were worth it: witness the fact they just rejected a $440 million offer from Blackstone/Hipgnosis Songs Capital (via Mercuriadis/HSM) for 29 of HSF’s catalogs… for a price that represented a 26% premium on the original fee that Mercuriadis paid to acquire them for HSF in the first place.

In addition, HSF’s top-line financials (before focus shifted to the irritation of a halted October dividend and other board wobbles) look solid: In July, HSF announced its strongest-ever annual fiscal results, with like-for-like revenues up 10.9% YoY.

Last point: HSF shareholders will appreciate that, by firing Mercuriadis, they invite the outside possibility of a ‘Taylor Swift crisis’ – i.e. songwriters with whom Mercuriadis has struck deals (from Neil Young, to Chrissie Hynde, The-Dream, the Chili Peppers, Lindsey Buckingham, Nile Rodgers et al) going public with potential anger over HSF trying to separate Mercuriadis from repping their assets.

Inevitably, such a scenario wouldn’t be great news for HSF’s share price.

Step 3: You’ve got to admit, though, that all of this HSF/HSC/HSM/Blackstone business looks a little nebulous…

Yes. There is certainly a fair accusation to be made at Mercuriadis about conflict of interest.

Since Hipgnosis Song Management began buying catalogs for Hipgnosis Songs Capital (i.e. with Blackstone’s money), HSF’s own buying spree has ground to a halt.

To be clear: said grinding to a halt has been caused by HSF being “fully invested”. While its shares trade at a discount the company is unable to raise more cash to buy stuff – and it’s prudently not looking to further expand its credit facility to do so in a high-interest environment.

But even if HSF did have a stack of new capital to spend, its HSM relationship is inarguably complicated by HSC’s presence. (See: the details of this 20% agreement between HSF and HSC).

The HSF board (and many shareholders) specifically asked for Blackstone to buy catalogs from HSF to allow for share buybacks. But in the harsh light of post-discontinuation, they may not adore this complexity.

Step 4: So they WILL fire Merck!

No, I doubt they will… primarily because his ‘call option’ leaves HSF vulnerable to losing capital growth, tied to streaming’s growth, that will come from assets that the company itself acknowledges are very valuable.

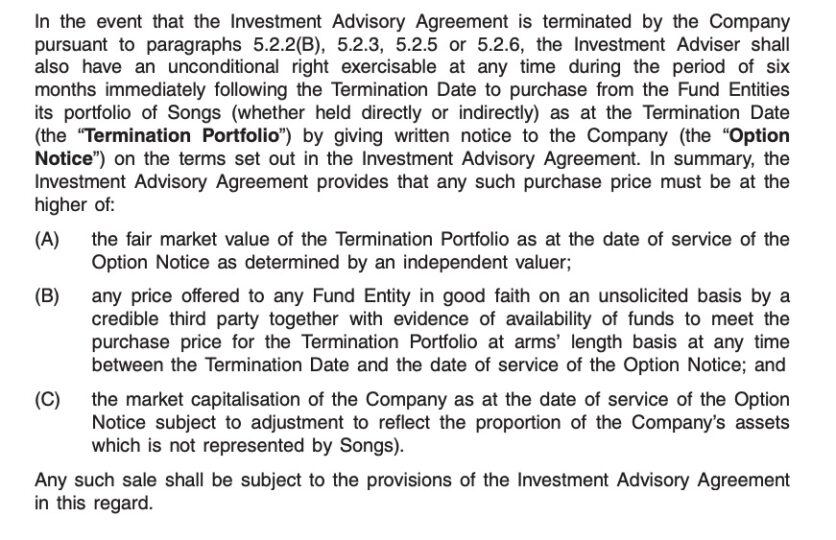

Have you looked into the finer details of Mercuriadis’ ‘call option’? I have.

It dates back to the prospectus of Hipgnosis Songs Fund, before HSF floated in 2018 and before any public shareholders invested a bean in the company.

Below is a summary of the ‘call option’, from that prospectus, in black and white.

Note: “[An] unconditional right exercisable at any time during the period of six months immediately following [HSM’s termination] to purchase from the Fund… its portfolio of Songs (whether held directly or indirectly).”

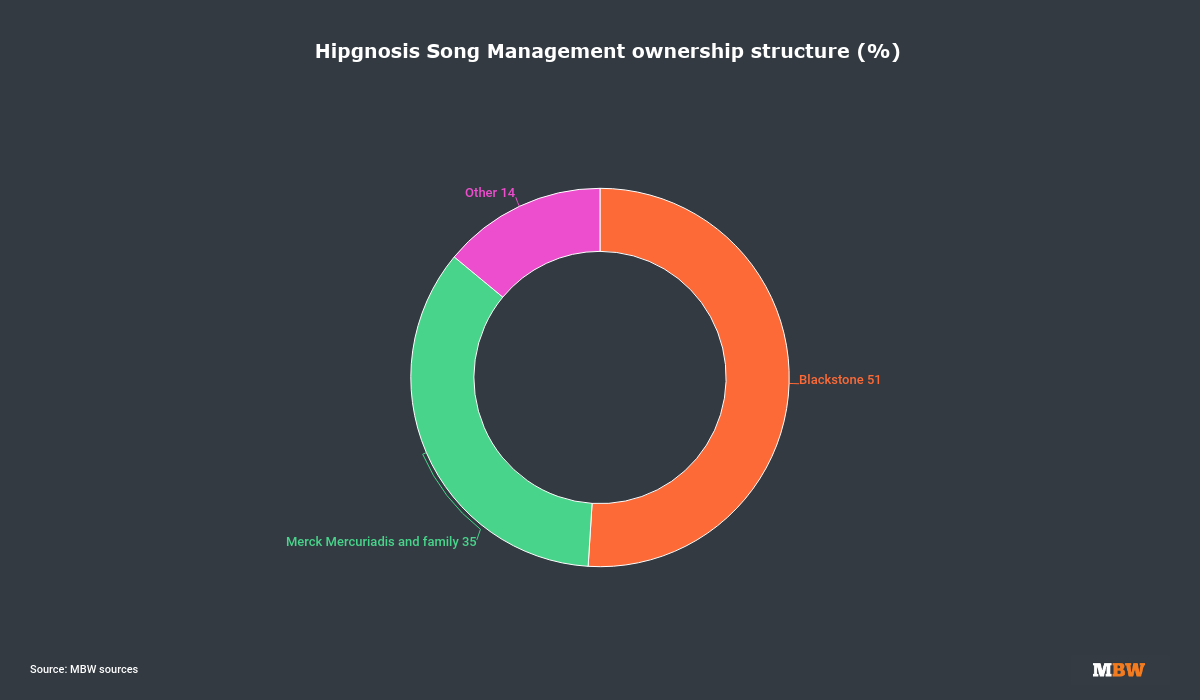

Hipgnosis Song Management (HSM) represents masses – as in, potential billions – of Blackstone dollars in the shape of Hipgnosis Songs Capital (HSC).

Blackstone is strategically invested in Hipgnosis Song Management too, owning just north of 50% of the investment advisory company.

So as soon as the HSF board fires Mercuriadis, you can bet he’ll just come and buy their assets, probably using Blackstone/HSC’s money.

Or, if HSC for whatever reason doesn’t have the appetite for the deal, or is only willing to part-fund it, Mercuriadis (and HSM) would be free to seek another third-party backer’s money.

If the HSF board chooses not to fire Mercuriadis, of course, the ‘call option’ is no threat to HSF. It stays in its box.

Step 5: Ah. But what if, following discontinuation, the HSF board de-lists Hipgnosis Songs Fund from the market, and sells it to, say, a major music company? The new owners would kick Merck out!

This is where things get fun.

Let’s imagine exactly what you just described happens for real. The board sells off Hipgnosis Songs Fund either at a price that Hipgnosis Songs Capital/Blackstone is unwilling to match, or they somehow just freeze out Merck Mercuriadis from the acquisition process.

In this scenario, let’s say Universal, Sony, or Warner becomes the owner of HSF.

What would these companies naturally do on day one of owning HSF? They’d sack Merck and HSM. Goodnight Vienna!

Except that sacking… would then trigger HSM’s ‘call option’… meaning that Mercuriadis and Blackstone would be able to buy HSM’s assets off the new owner… without that new owner being able to stop it.

A source previously involved in HSF at a senior level told MBW earlier this week: “When things were going great, five or so years ago, the [HSF] board waved Merck’s ‘call option’ request through without fuss.

“It’s laughable that the same board asked him to spike the same ‘call option’ the other week – and hardly surprising he told them no way.”

“When things were going great, five or so years ago, the [HSF] board waved Merck’s ‘call option’ request through without fuss.”

MBW source

Said the same source: “Merck has always maintained that he made sure he crossed the t’s and dotted the i’s so that when he told these songwriters he would represent their catalogs for the rest of his life, he would.”

Another source close to Hipgnosis Songs Fund’s initial IPO in 2018 comments, “Merck explained to shareholders at the beginning that if he was going to build a multi-billion dollar fund, he’d need to navigate some very emotional discussions with songwriters. If he was going to acquire catalogs from cultural giants like Neil Young – and Neil Young was the exact example he used at the time – he’d have to make a deal for their ‘metaphorical children’.

“That was the justification for his ‘call option’: To [buy catalogs] directly from people like Neil Young, Merck would have to look artists in the eye and promise them that he’d never have to give up the management of their songs, regardless of whether the capital behind Hipgnosis ever changed.

“Shareholders agreed to Merck’s ‘call option’ before they ever invested a pound in Hipgnosis. It’s been in the company’s prospectus spelled out since day one.”

Step 6: Couldn’t Hipgnosis Songs Fund get legal? Try to weaken Merck’s ‘call option’, or terminate HSM, that way?

I mean, yes, of course, they could always try. And what a flurry of exciting headlines that would bring to MBW 😃!

But it would also be extremely messy… and, assuming Mercuriadis has run his ship diligently, it would likely be unsuccessful.

There are boilerplate provisions in HSM’s agreement with HSF, as noted in the original HSF prospectus, that cover HSM’s contract being terminated if HSM commits the usual standout fiscal sins (wilful misconduct, fraud, breaches of obligations etc.).

There’s also a boilerplate clause in there about HSM being able to be chopped by HSF if there’s a ‘Key Person Event’ (i.e. if Merck Mercuriadis can no longer act as CEO of HSM).

But here’s what we know: (a) Mercuriadis’ ‘call option’ has been part of HSF’s prospectus before anyone was asked to invest in the firm; and (b) That same ‘call option’ is clearly deemed rock solid enough for HSF’s board to publicly admit – in the past few weeks – that they asked Mercuriadis to revoke it. (He said no, obvs.)

Here’s what else we know: Hipgnosis Songs Fund, with a near-maxed-out RCF in a tough interest rate environment, probably doesn’t have a barrel-load of cash right now for a big legal fight (esp vs. an opponent potentially funded by Blackstone). Any change in manager would also require approval from the banks behind HSF’s debt, who, it’s understood, have faith in Mercuriadis.

Ultimately, a peaceful solution will surely be the preferred outcome for all parties.

As Mercuriadis said in his statement yesterday “… we look forward to working with a new Chair and reconstituted Board during this period to ensure that the Hipgnosis Songs Fund delivers for its shareholders“.

Step 7: Is That your gut instinct? That HSM will remain adviser for HSF, working with a new board to shore up a share price that’s plummeted? Even with HSF’s tough debt-payback vs. dividends balance to strike?

No, that’s not my gut instinct.

Mercuriadis has stated publicly that he would like to see HSF shareholders benefit from the capital growth that will come with HSF’s owned catalog in years to come. He’s also talked about his gratitude to those shareholders for making the establishment of songs as an asset class possible.

Regardless of all that, my gut instinct is that those shareholders will eventually ask Mercuriadis/Blackstone to buy Hipgnosis Songs Fund, or buy the full HSF catalog, within the next 12 months.

I have zero knowledge of whether or not this will come to pass, or if such discussions have even been flirted with to date.

It just feels like the neatest possible conclusion for all. It’s an outcome in which everyone currently invested in HSF, either via shareholder equity or sweat (HSM included), can walk away with a degree of satisfaction.

The price for that deal, I would guess, will fall somewhere between HSF’s public share price and the now-infamous ‘operative NAV’ (i.e. private valuation) put on the HSF portfolio.

In March, that operative NAV stood at USD $2.316 billion.

Step 8: Your suggested outcome would surely be a surprise, though? Seeing as HSF shareholders just voted overwhelmingly to reject Blackstone/HSC’s $440 million offer – which came via Merck – to buy 29 of HSF’s catalogs. The consensus is that Merck’s offer significantly under-valued those assets, coming as it did at a 17.5% discount on the market worth of the catalogs as per Citrin Cooperman’s estimate.

There’s a whole other article to be written about this, digging deeper into the ‘true’ multiple that Concord is paying for HSF’s rival, Round Hill Music Royalty Fund Ltd (see details of that here) vs. the multiple implied by HSM’s $440 million offer.

But for now I’ll stick to this: there’s a bit of ‘having cake and eating it’ within your points.

For some time now, Hipgnosis Songs Fund’s independent valuer, Citrin Cooperman, has come in for flak (from those with a bearish view on Hipgnosis) for the 8.5% discount rate used in CC’s valuations of HSF.

Despite cost of capital and interest rates leaping up and up, Citrin Cooperman (formerly Massarsky Consulting) has resisted the idea of raising that 8.5% to, say, 9% or 9.5%, at every turn.

There is fierce debate out there over this decision: For example, see Round Hill Music Royalty Fund Ltd’s use of a second valuer (FTI), in addition to Citrin Cooperman, when getting its own valuation report done in April.

For a calculation to determine the Round Hill fund’s value (for the purpose of financing with bank debt), Citrin Cooperman stuck with a discount rate of 8.5%.

FTI, on the other hand, used a higher discount rate, of 9.25%.

(FTI used a lower rate when calculating the fund’s worth for ABS financing.)

Citrin Cooperman’s 8.5% discount rate is one of the reasons, says HSF critics, why there’s an such unhealthy gulf between Hipgnosis Songs Fund’s share price/market cap and its ‘Operative NAV’ today.

Yet if that 8.5% discount rate went up, as some HSF critics suggest it should in the current fiscal environment, then as a direct result the independent value of HSF would go down.

And as a result of that, the now-rejected $440 million offer from Hipgnosis Songs Capital/Blackstone for the 29 catalogs of HSF would suddenly look significantly rosier (vs. the re-valued worth of HSF’s assets).

Furthermore, during HSF’s ‘go-shop’ period, HSF’s board and financial advisor JP Morgan couldn’t find any other party willing to better HSC’s $440 million offer for the assets.

That’s despite 17 companies having a little kick of HSF’s tires at the start of the ‘go-shop’ process.

(Some sources suggest the ‘go-shop’ contained offputting ‘poison pills’ for rival bidders vs. Blackstone’s $440 million offer, not least the fact that Blackstone/HSC had a ‘matching right’ to gazump any third-party bid that came forward. Other sources close to the ‘go-shop’, however, argue it was a legitimate process, and that in the music industry ‘matching rights’ are commonplace during the acquisition tender of large catalogs. Without ‘matching rights’, they argue, buyers would obviously be unwilling to show their price to the open market – and their competitors.)

Will HSF shareholders end up regretting that they passed on HSC/Blackstone’s $440 million offer – which equated to a multiple of 18.3x historical Net Publisher Share (NPS) of the catalogs in question?

Maybe. Maybe not. That all depends on where the public value of Hipgnosis Songs Fund moves next.

As things stand, expect Merck Mercuriadis, with that all-important ‘call option’ in his back pocket, to have a front-row seat for the next chapter in this story.