Thomas Coesfeld is the Chief Financial Officer of BMG. Here, in an exclusive MBW op/ed, Coesfeld argues that the correct response to booming global music industry revenues should be improved service to artists and songwriters – rather than a money-no-object pursuit of market share…

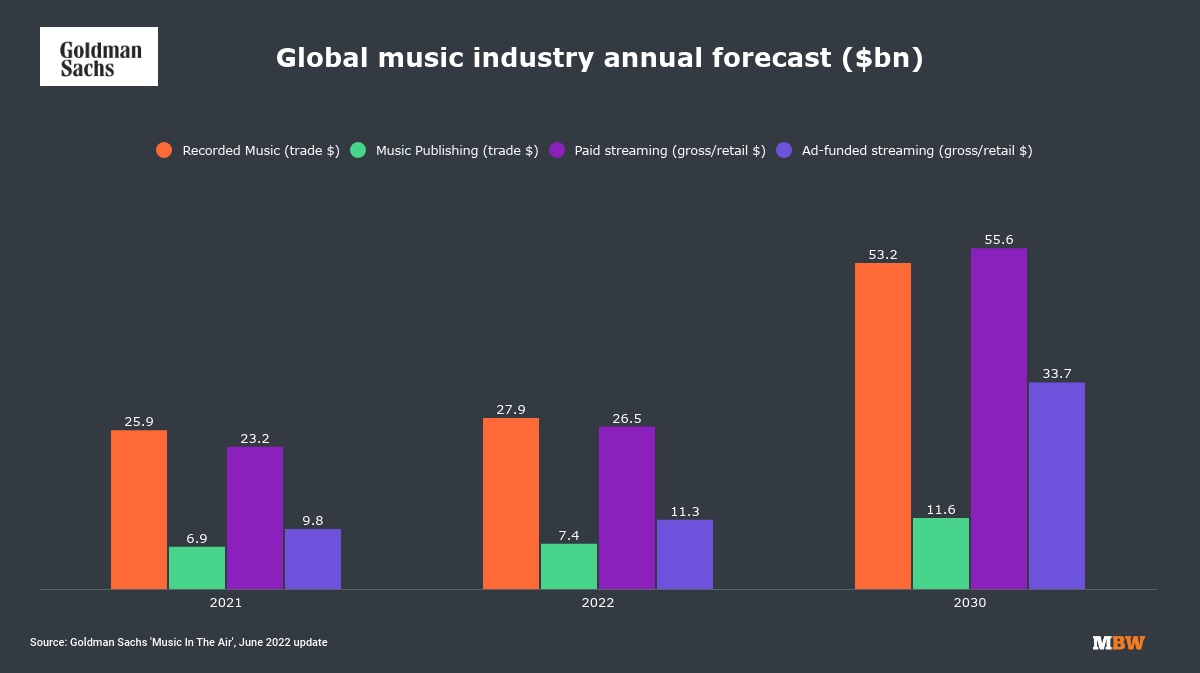

June 13, 2022 was a big day for finance teams across the music industry. It was the day Goldman Sachs released its revised forecasts for the music industry with new numbers suggesting the recorded music market will double by the end of the decade.

At BMG, as no doubt elsewhere, internal forecasts were rapidly being upgraded. Those with long memories who saw the vinyl LP eclipsed by compact discs selling for twice the price could be forgiven for thinking history was repeating itself. Happy days!

However, despite the rosy picture painted by Goldman’s forecasts, there are grounds for a little humility. Nothing in those forecasts suggests the predicted growth will be in any sense thanks to the collective efforts of music companies themselves.

They are not based on record companies suddenly getting better at their jobs and signing more or bigger hits; they are a by-product of a fundamental shift in the way consumers choose to consume music, driven by the investment and innovation of DSPs.

It is reasonable therefore to discuss what the correct response is to this stroke of good fortune.

If the past is any guide, the default response will be to do more of the same – only more expensively – in the pursuit of market share. It is hard to argue that a battle for market share benefits either artists or songwriters. History suggests it doesn’t do much for shareholders either.

On the basis of the old truism that the best time to fix the roof is while the sun is shining, I would argue that the real battleground should not be on marketshare, but on service and value-add to musicians and rightsowners.

“Better aligning the interests of music companies with the artists and songwriters they serve is, I believe, the single most important transformational opportunity offered by streaming.”

Improving service levels, better aligning the interests of music companies with the artists and songwriters they serve is, I believe, the single most important transformational opportunity offered by streaming.

The first phase of that transformation focused on fairness and transparency, a recognition that the historic relationship of music companies to musicians was unbalanced and often unfair and that simply translating the contractual terms of the analogue era to streaming was inappropriate and unsustainable.

Much of the industry has now accepted in word if not always in deed that fairness and transparency are non-negotiable in the streaming age.

The second phase, which we are currently in the middle of, is the growing understanding that music companies are now essentially service businesses to musicians. They are no longer the principals in the market. They work for the artists and songwriters who actually make the music.

Progress here is slower. Understandably the larger the company, the less keen they are to accept that their historic role as the drivers of the business is over. But that is the unavoidable logic of the technology.

The third transformation arising out of the previous two, we believe, will be a focus on the active revenue management of recorded and publishing rights, minimising inefficiencies in the revenue chain and maximising income to rights owners.

The key driver for this will be the increasing number of high-value catalogues held outside the traditional music companies – either owned by artists themselves or, increasingly, by investors.

“Investors who have committed literally billions of dollars to acquiring music IP will not tolerate the degree of revenue leakage, the multiple commissions, admin fees and grindingly slow processes still common in this business.”

Certainly investors who have committed literally billions of dollars to acquiring music IP will not tolerate the degree of revenue leakage, the multiple commissions, admin fees and grindingly slow processes still common in a business which has still yet to made the leap from an analogue to a digital mindset.

It demands a focus on music industry structures and overhead on the one hand and processes on the other. It will put an increasing premium on the most under-appreciated services of the music industry – copyright, royalties, income tracking. They may not have the glamour of A&R, marketing or synch, but they will be core differentiators in the years ahead.

We would rather pin our hopes on differentiation and a clear strategy rather than simply hoping we can coast our way to increased revenues on the back of market growth. There is so much work still to be done.

In a recent pitch to a songwriter we reviewed a potential client’s Top 30 tracks on YouTube – only three of them were correctly registered and claimed by their current music publisher.

This is not an isolated case. Striking deals with digital platforms is one thing; knowing how then to work with them successfully is something else entirely. It is these areas of revenue optimisation and income tracking assurance where we believe the greatest opportunity lies.

We must ensure that as much as possible of the top-line growth forecast by Goldman Sachs is captured and passed on rather than squandered on objectives such as market share which mean nothing to the musicians who ultimately pay the bills.

That is the best way for us to repay the faith of the artists, songwriters and of course shareholders who ultimately make the work we all do possible.

To put it another way, if that is not our priority, artists and songwriters and rightsowners could be forgiven for asking what is the point of music companies at all?Music Business Worldwide