The MBW Review gives our take on some of the music biz’s biggest recent goings-on. This time, we hammer the calculator to work out what each of Spotify‘s 48m subscribers were paying by the end of 2016. The MBW Review is supported by FUGA.

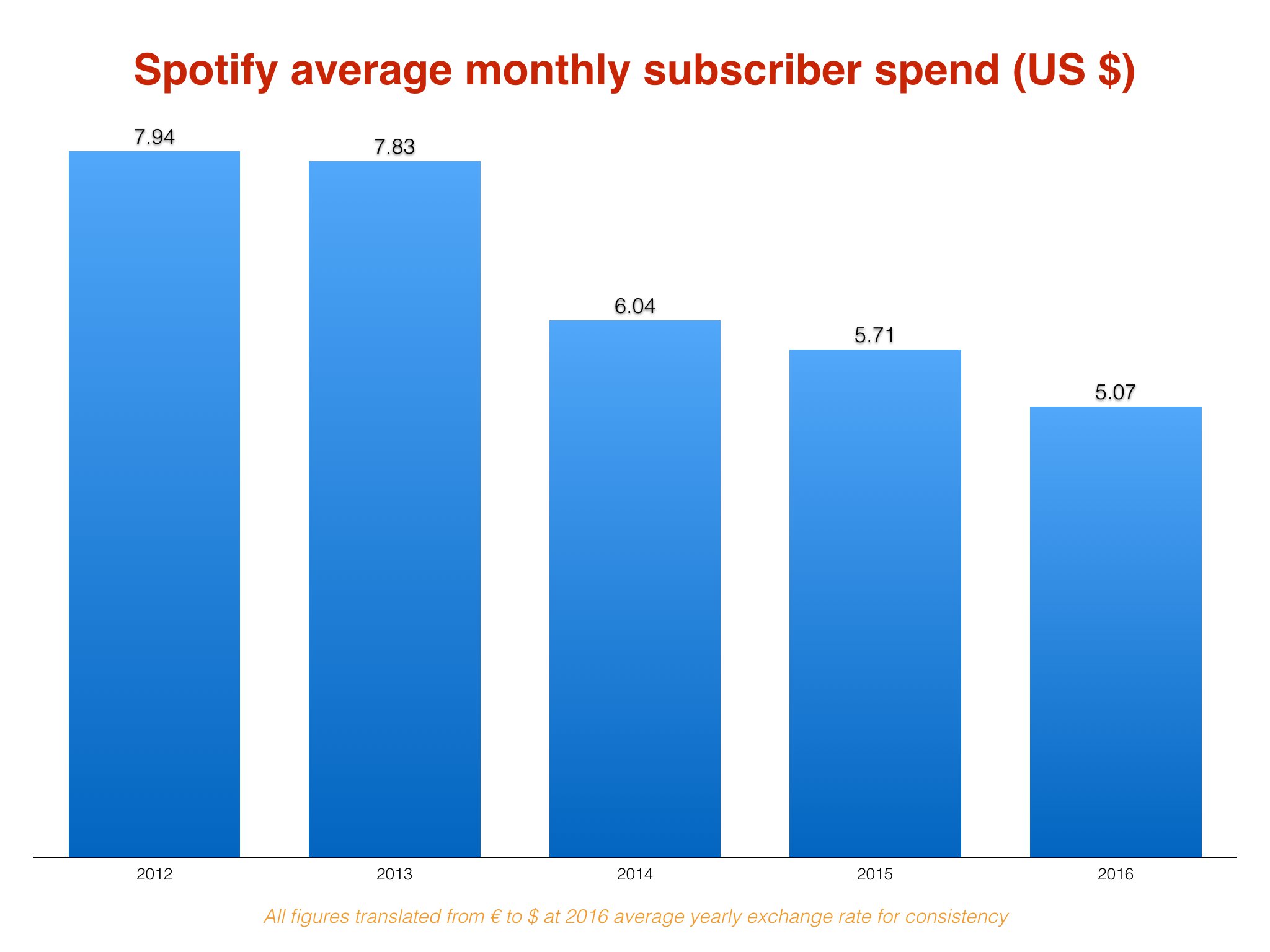

The average amount of money being paid for an annual Spotify subscription has fallen by more than US $30 since 2013.

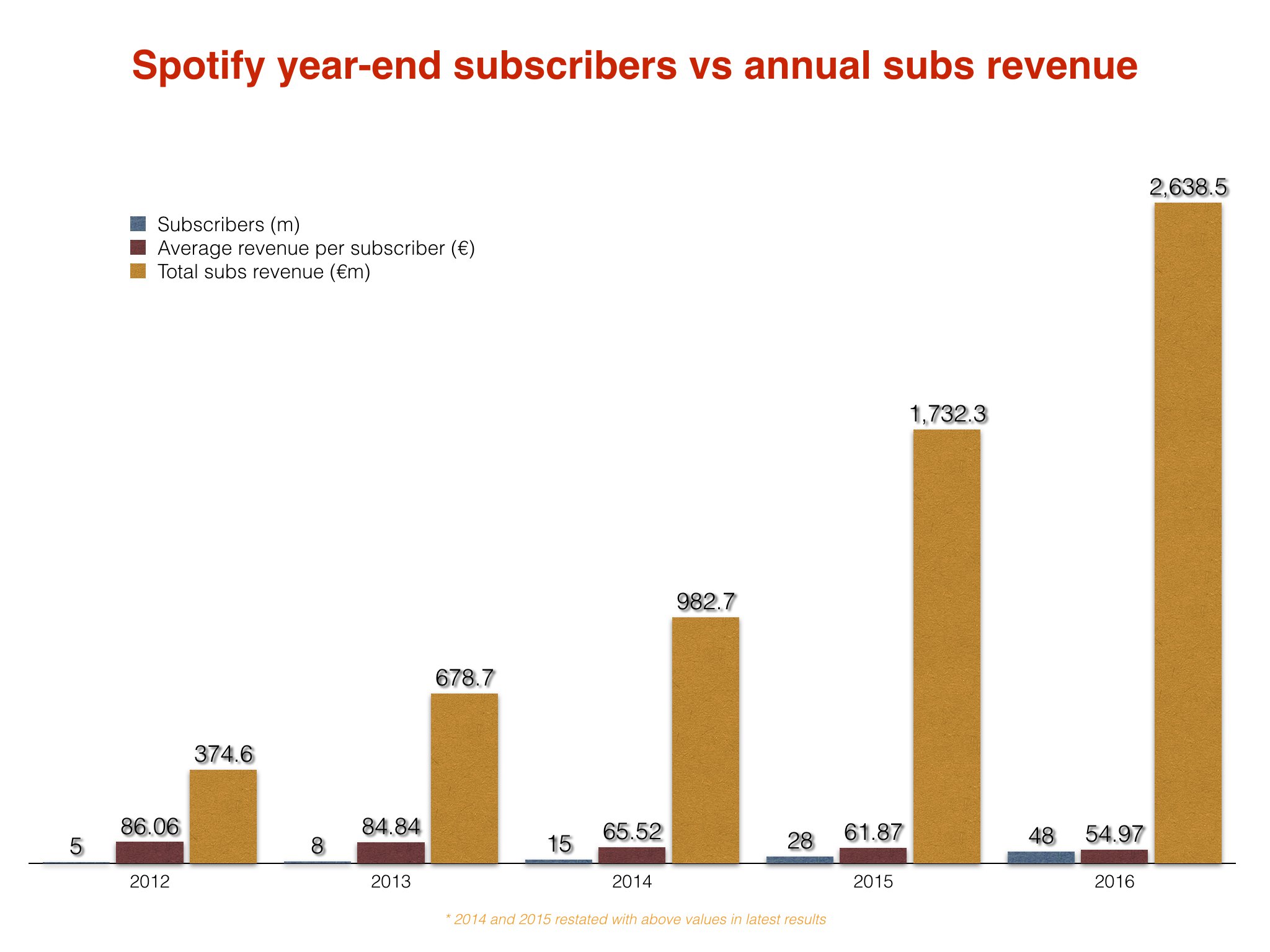

According to Spotify’s latest annual report, its subs revenue rose by over $1bn in 2016 – up 52% year-on-year to €2.64bn ($2.9bn).

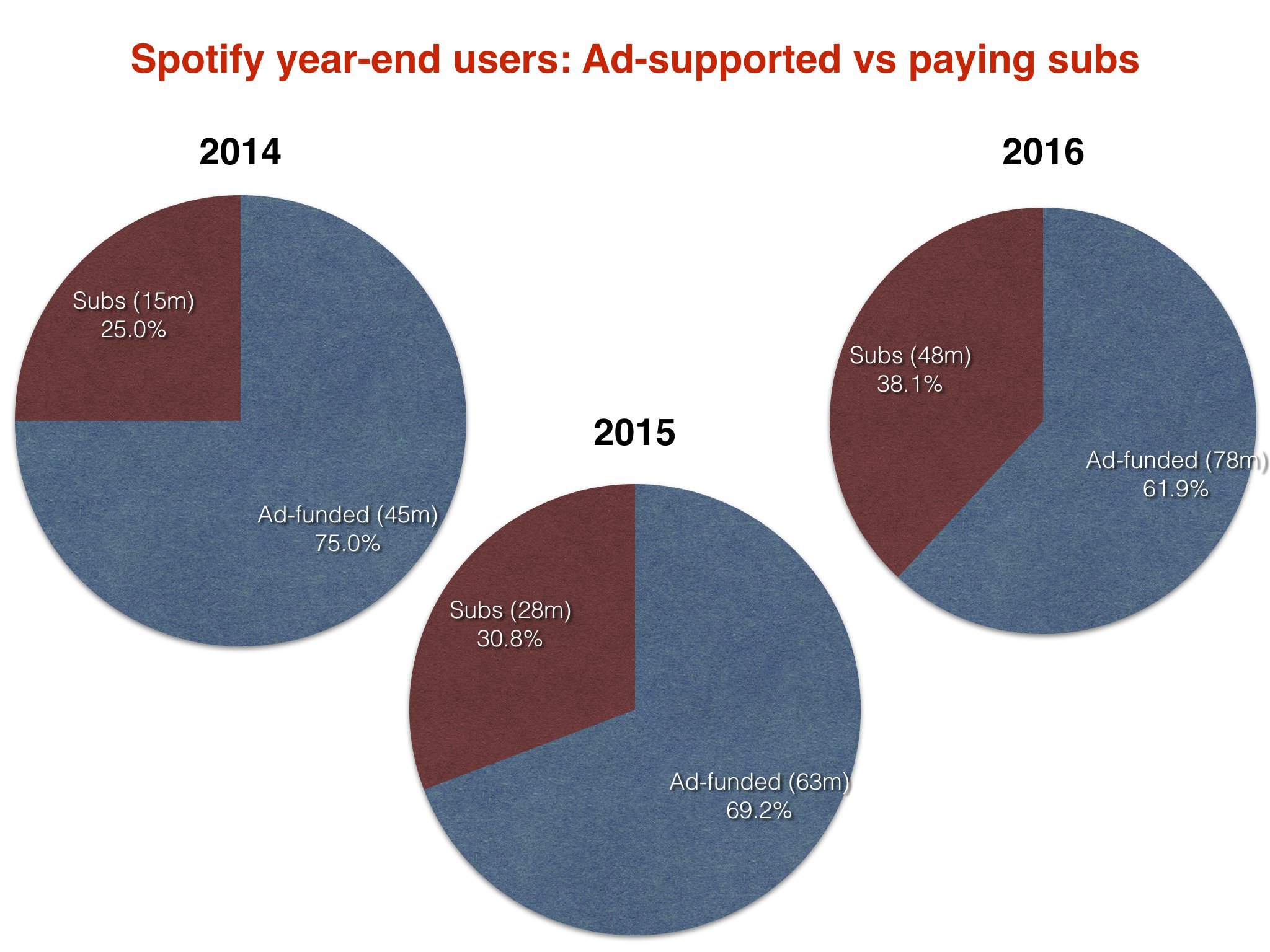

Meanwhile, the company’s total year-end subscriber base jumped by a record amount – up 71% from 28m in 2015 to 48m last year.

Before we get into what that means in terms of individual subscribers, a small caveat: by dividing the total year-end subscriber base by the annual subscription revenue, we get a useful ARPS (Average Revenue Per Subscriber) figure.

However, this number is inevitably a lower-end estimate – cross-pollinating, as it does, Spotify’s total revenue over 12 months with a subscriber base at its highest point in the year (ie. the end of December).

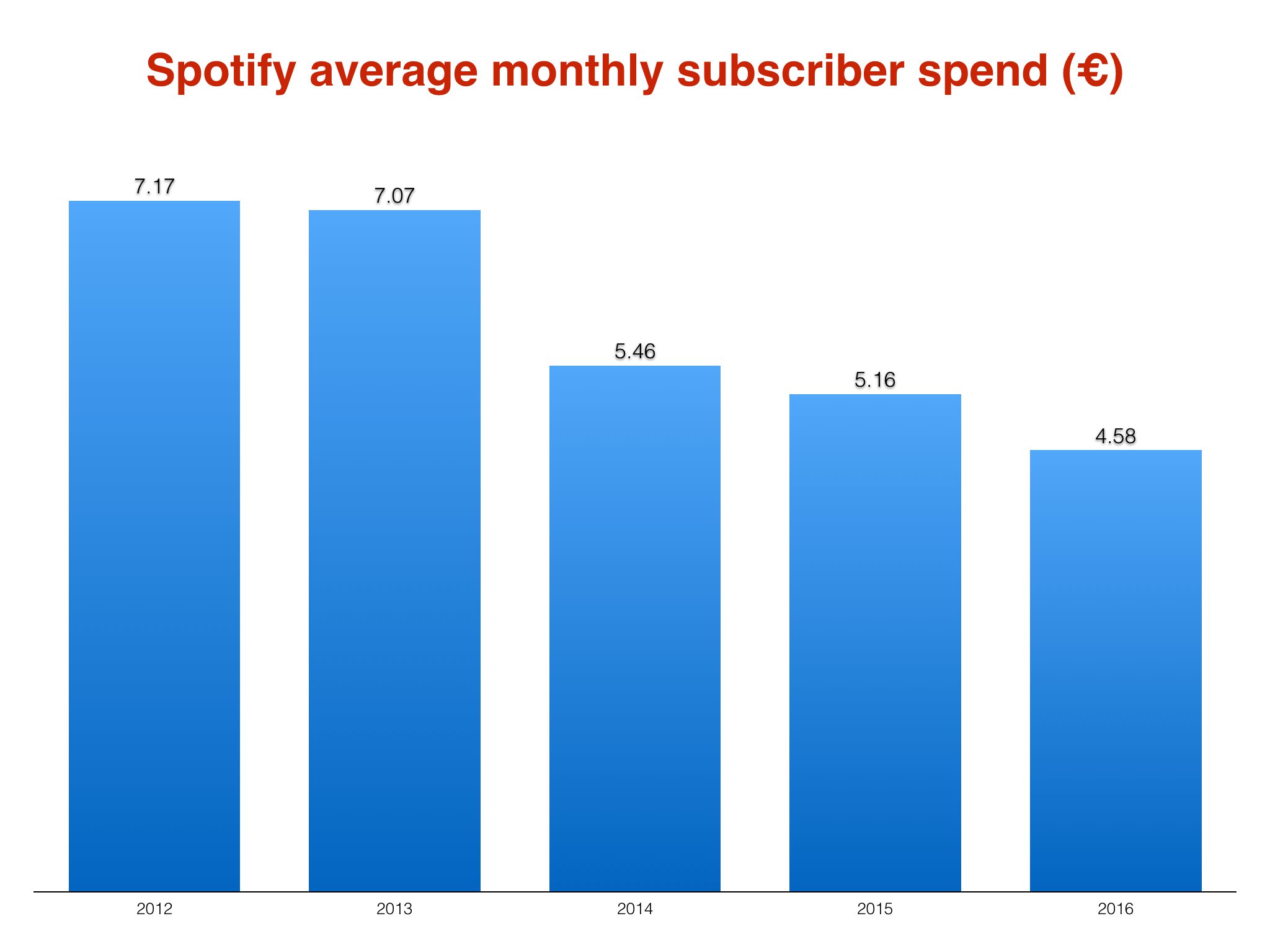

Using this calculation, we can see that in 2016 the average Spotify subscriber paid €54.97 (US $60.84) – or €4.58 ($5.07) per month.

This was down 11% on the €61.87 ($68.48) ARPS seen in 2015, which worked out to €5.16 ($5.77) per month.

Back in 2014, the average subscriber paid €65.52 ($72.52) annually, or €5.46 ($6.04) per month. It’s since fallen by 16%.

There are a number of reasons for this drop in average per-user subscription spend – not least pricing and currency fluctuations in certain territories.

For example, Spotify expanded into Indonesia last year, where a premium subscription will cost you Rp 49,990 per month – the equivalent of US $3.80, or $46 a year. (Worth noting that Spotify’s biggest expansion move last year – its entry into Japan – came with a monthly premium charge of 980 Yen, or close to US $10 a month. )

In addition, Spotify’s ARPS has been dragged down by aggressive price promotions, such as the three-months-for-$1 deal it regularly re-launches to try and tempt in new paying customers.

And then there’s Spotify’s global family plan, which became significantly cheaper last year in order to compete with Apple’s more competitive pricing.

Since May 2016, a family account on Spotify has cost $14.99-a-month in the US. Previously, if such a family bundle was used by the maximum allowance of six people, it would have cost $34.99-a-month.

In its end-of-year filings last week, Spotify admitted: “Our launch of the global new family plan resulted in strong subscriber growth. However. this strong growth did not materially impact revenue performance in the year as it was partially offset by the price reduction on the existing family plan subscriber base.

“We also had a strong intake of our holiday and summer campaigns. adding subscribers worldwide, in line with 2015.”

In fact, Spotify had its strongest annual subscriber growth of all time last year – with the 20m year-on-year jump in paying customers to 48m outperforming 2015 (+13m), 2014 (+7m) and 2013 (+3m).

However, a byproduct of this rapid rise was a cheaper average subscriber cost.

Rewind the clock to 2013, when Spotify’s year-end subscriber count was at 8m – some 40m smaller than 2016’s equivalent tally.

That year, the firm’s Average Revenue Per Subscriber (ARPS) stood at €84.84 ($93.91) annually.

2016’s equivalent figure was 35% smaller, with approximately $33 less a year spent per subscriber on average.

Although Spotify has never officially reduced its monthly subscription cost from $9.99, this number has now clearly fallen regardless (in average per-head terms) very near to the $5-a-month figure more commonly associated with the idea of ‘mid-tier’ streaming pricing.

How significant is the reduction in this ARPS figure to Spotify’s bottom line?

Put it this way: Spotify suffered an annual operating loss of €349.4m ($387m) last year, widening by 48% on 2015.

If Spotify’s average subscriber in 2016 was still paying the same amount they were in 2013 – $33 more per person across the year, remember – then the company would have generated an additional $1.58bn, resulting in an operating profit of approximately $1.2bn.

Even in 2015, the average Spotify subscriber was paying approximately $4.20 more across the year than they were in 2016.

Had Spotify been able to maintain this ARPS in 2016, it would have generated an additional $202m, knocking last year’s annual operating loss down to a far-more-manageable-looking $185m.

Or to switch things on their head: Spotify would have needed $8 more per subscriber across the whole of last year to wipe clean its 2016 operating loss completely.

That would have only meant an additional $0.67 per subscriber, per month.

Subscription provided 89.9% of Spotify’s total revenues last year, with its ad-funded tier contributing €295m ($330m), or 10.1% of the total pie.

Interestingly, the Average Revenue Per User (ARPU) of Spotify’s ‘free’ users on its ad-supported tier grew slightly in 2016 – as ad-related income outstripped user increases.

Spotify’s 78m ‘free’ users at the end of last year generated approximately €3.78 ($4.18) each across 2016 – a monthly average of €0.32 ($0.35).

In 2015, Spotify’s 63m ‘free’ year-end users generated approximately €3.11 ($3.44) each in the year – a monthly average of €0.26 ($0.29).

In positive news for Daniel Ek, these figures demonstrate Spotify’s best ever free-to-premium conversation rate – with 38.1% of 2016’s 128m year-end users paying for Premium, compared to 30.8% in 2015 and 25% in 2014.

Conclusion: the bigger Spotify gets, the greater the percentage of its users are paying for Premium – but the smaller the average amount of money they’re having to shell out to do so.

(All US $ figures above translated at 2016 yearly average exchange rates for consistency in comparison.)