“The major labels are losing market share on Spotify.”

So reads the headline (or variations of it) on article after article from the past several years.

The scale of ‘DIY’ music uploaded to streaming services has skyrocketed, and the three major record companies – Universal Music, Sony Music, and Warner Music – have seen their market share eroded, slightly but consistently, year-over-year.

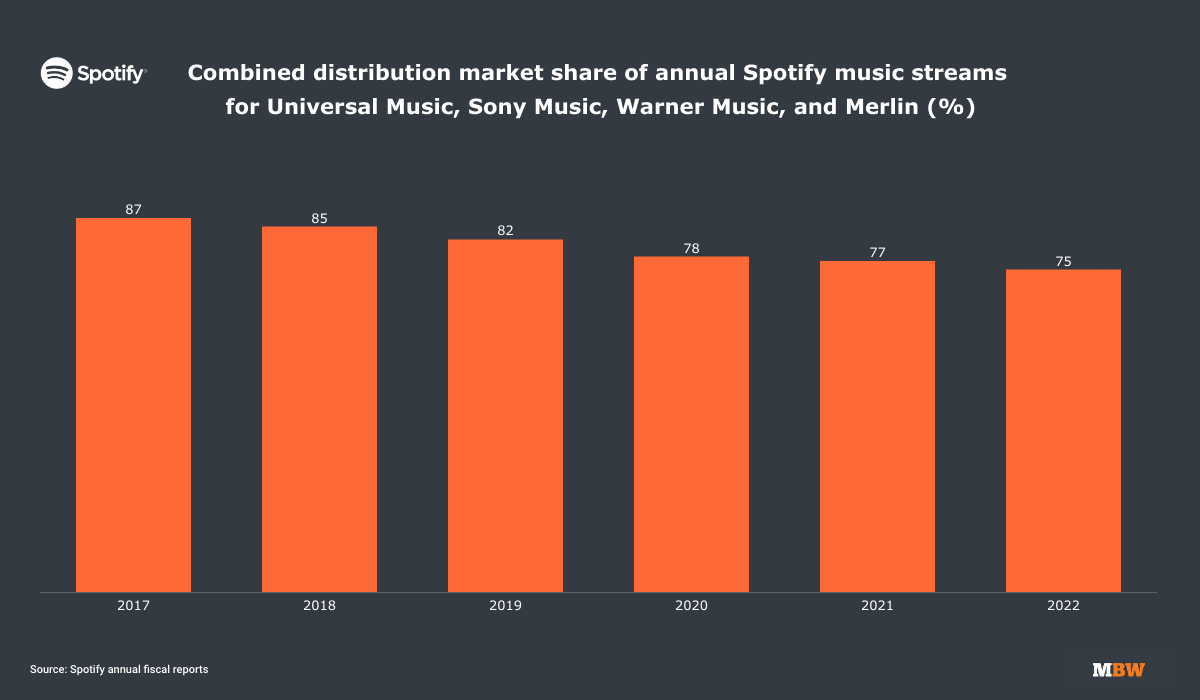

Spotify, in its latest annual investor report, has – as previously reported by MBW – divulged that “majors-plus-Merlin” market share on its platform totaled 75% in 2022, marking a two-point decrease from the year prior.

This share has decreased every year since 2017, when it stood 12 points higher (at 87%) than it does today, as seen above.

The “majors-plus-Merlin” share denotes any artist who is ultimately distributed either via the three major record companies (or their indie distie subsidiaries), or via Merlin members including the likes of Beggars Group, [PIAS], and Secretly Group.

(MBW has clarified that Spotify’s non-major/Merlin figures above include distributors such as TuneCore, CD Baby, and DistroKid, despite DistroKid being a Merlin member for some service deals.)

This spells unhappy news for the ‘majors’, who have historically been benchmarked against one another, and the industry at large, by market share above any other metric.

The trend can largely be explained by the explosive growth of the independent and in particular ‘DIY’ artist sector in recent years.

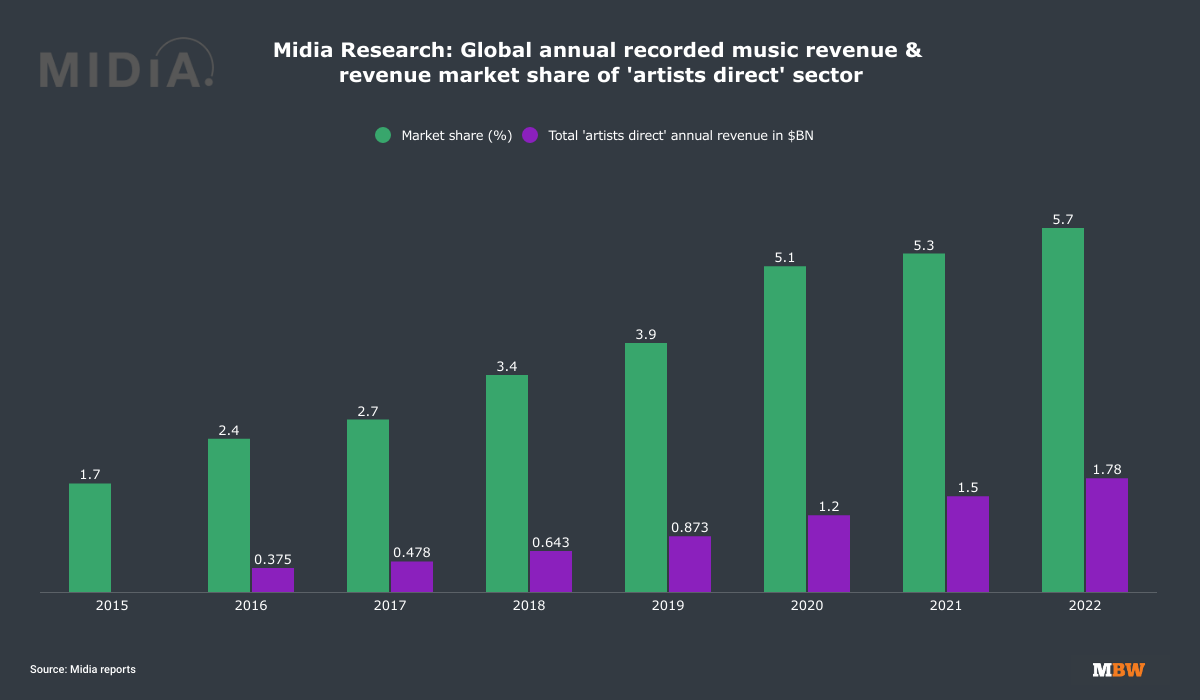

Globally, over the year 2022, MIDiA reports “artists direct” (i.e., self-releasing artists) held an impressive recorded music market share (in worldwide recorded music revenue terms) of 5.7%.

This market share figure has increased each year since 2015, when it was only 1.7%. In other words, the market share of ‘artists direct’ has more than tripled in 6 years.

In absolute dollar terms, meanwhile, the “artists direct” sector’s total revenues quadrupled from 2015-2022, up from $375 million (2015) to a whopping $1.78 billion (2022; MBW has confirmed this figure with Midia to two decimal places).

On the one hand, this trend seems somewhat unavoidable for the majors, given the sheer and rapidly growing number of non-major-distributed tracks that are uploaded with each passing year.

And, of course, it’s also worth noting the majors are sustaining double-digit percentage growth in revenues each year despite any erosion they are seeing to their combined music streaming market share.

On the other hand, this trend also syncs up with a longstanding shift in perceptions among independent artists – one which is perhaps in some ways a broader threat to the majors.

Artists with large ambitions were, at one time, pre-streaming and iTunes, virtually forced to partner with record companies if they were to have any hopes of reaching a wide-scale audience (mass-manufacturing physical records was prohibitively expensive, not to mention marketing and so on).

Nowadays, the majors represent one pathway for aspiring career artists, but not necessarily the most attractive option for all, given independent routes are more accessible than ever.

One recent MIDiA survey of hundreds of independent artists concluded that over half of them wanted to: “Become respected and recognized in [their] scene” (53%); “be a successful touring artist” (51%); and “build up a loyal fanbase of any size” (50%).

How many of them wanted to eventually sign with a major label?

Less than one in six – only 16%.

(9% wanted to instead sign a label services deal, while 12% wanted to sign with an independent label.)

It seems many independent artists, including some very successful ones, have decided that the conventional major label pathway is simply not for them.

To address this, each of the three majors has by this point made significant investments into independent artist-friendly alternatives to their traditional labels:

- Universal Music has Virgin Music Group, housing Ingrooves, the independent distributor fully acquired by UMG in 2019 for around $100m;

- Sony Music has its label services arm The Orchard as well as AWAL, which it famously acquired for $430m in H1 2021; and

- Warner Music has its Alternative Distribution Alliance (ADA), as well as Level Music, a DIY distributor that is a direct competitor to the likes of TuneCore and DistroKid.

One can argue that these ‘label services’ operations have gone – in relatively short order – from just one of the majors’ business lines, and a relatively small one at that, to playing a central role in their futures.

Now more than ever, many artists still want to harness the influence, global reach and expertise of the majors, but only on terms that enable them to keep ownership of their copyrights – and only sign them away on relatively short-term licensing or distribution agreements.

As the era of the megahit dissolves, potentially for good, this author believes the best path for the majors to maintain streaming market share will be through alternatives to their powerhouse ‘name brand’ labels.

MAJORS’ LABEL SERVICES OPERATIONS GROWING IN MARKET SHARE AND STRATEGIC IMPORTANCE

Nowhere is the growing importance of each major’s label services operation to its overall market share more apparent than with Sony and The Orchard.

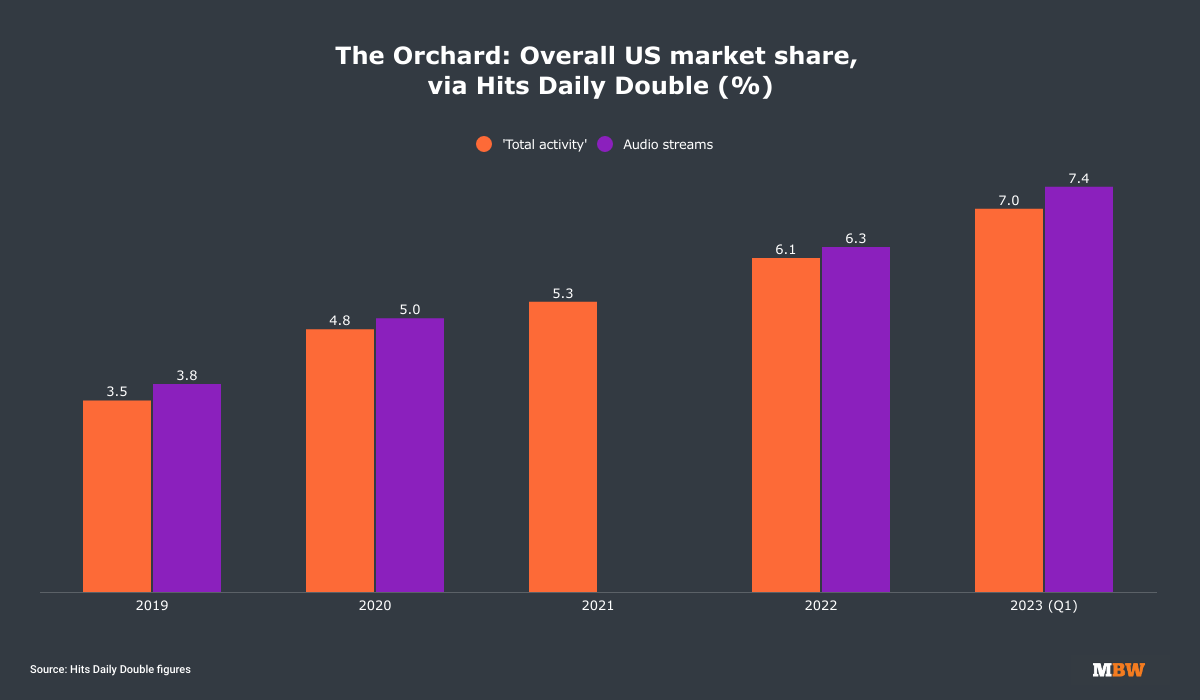

From 2019-2023, the latter’s market share in the United States has doubled.

According to Hits Daily Double reports, The Orchard – partly thanks to successes with artists such as RAYE and Bad Bunny – claimed a 7.0% ‘total activity’ market share in the US in Q1, taking into account all releases (‘Overall’).

That left it as Sony Music’s single biggest entity in the period, above powerful frontline labels such as Columbia (6.6%) and RCA (5.6%).

The growth in The Orchard’s ‘total activity’ US market share in recent years has been a notable trend:

- In FY 2019, reports Hits, it stood at just 3.5%;

- In FY 2020, it grew to 4.8%;

- In FY 2021, it hit 5.3%;

- And in 2022, it rose to 6.1%.

In terms of just ‘frontline’ releases – i.e. online music issued within the prior 18 months – The Orchard claimed an even bigger US ‘total activity’ market share in Q1 2023, at 8.3%, says Hits.

Essentially, an entity like The Orchard offers artists like Bad Bunny – arguably the biggest artist in the world at this time of writing – the ability to join a major, Sony Music in this case, while staying signed to an independent label (Rimas Entertainment).

In other words, internal label services companies like The Orchard allow superstar-level artists to access the resources of a major frontline label – financing, dozens of departments: marketing, digital, radio, PR, etc.– without having to sign a traditional recording contract.

In Bad Bunny’s case, on Rimas Entertainment, which struck a label-wide deal with The Orchard in 2021, the artist last year generated more streams than any other on Spotify – a huge boon to Sony’s market share.

With the new re-focus on the independent artist and label segment of the music business, it might not be surprising to see Universal and Warner’s label services companies eventually overtake their traditional labels, too, given enough time.

Facing the future

If the majors continue to lose market share to DIY artists on Spotify and other music streaming platforms, it will not come without a fight.

New times have called for new business practices, and to their credit, the major labels have taken some genuinely historic, landmark steps towards creating a fairer future in recent years – like committing to pay through royalties to unrecouped ‘legacy’ artists.

New major label deals are changing, too, and certain ones – depending on the size and leverage of the artist – are being offered now that would rarely if ever have been seen in the physical era: License deals under which artists retain ownership, 50-50 or better profit-sharing rates, full creative control, and so on.

There will always be a place for the major record companies, but as dynamics shift, their premium frontline labels can only take Universal, Sony, and Warner so far.

In a world where longtail is king, and superstar artists are simply not as popular as they once were, the label services and distribution worlds are where the majors will have to focus to retain their market share throne.Music Business Worldwide